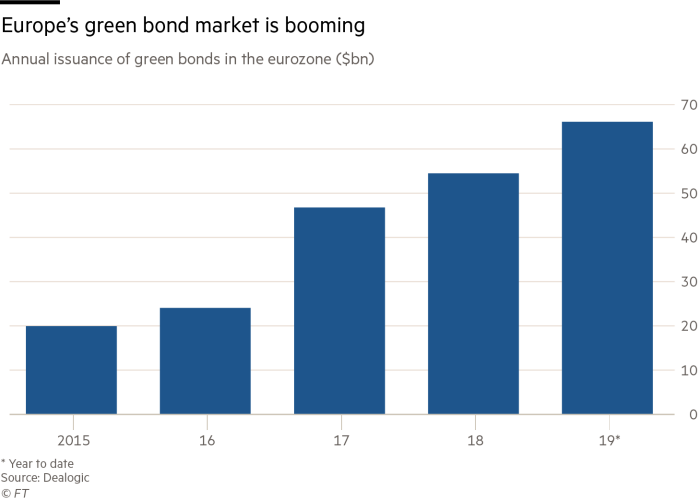

The world’s first ever green bond was issued by the European Investment Bank (EIB) in 2007. Since then, green bonds have gained traction with 262 billion USD worth of green bonds being issued in 2019 (according to the Climate Bonds Initiative). However, the Green Bond market accounts for only 2% of the overall bond market according to Refinitiv, a global provider of financial data. This article discusses the different ways of expanding the share of green bonds in the global bond market.

Let us first understand the theory behind green bonds:

Green bonds are just like any other bond. They are a form of loan where investors lend their money to the issuer of the bond in return for interest on the money lent. These interest payments are paid periodically and at the end of these periodic cycles (maturity date), a final sum (usually determined before investor invests) is paid to the bondholder.

However, there is one extra condition: the money lent by investors to issuers must fund projects that benefit the environment or help achieve sustainability goals; for example, switching energy sources from fossil to renewables or funding R&D for Carbon Capture & Storage. This source of finance helps address the physical and transition risks of Climate Change1 while increasing the levels of sustainable activity in the world economy.

Another significant advantage of the green bond is the introduction of a profit motive into the hitherto altruistic narrative of environment protection. Green bonds provide a tangible incentive to address climate change and make green activity profitable, leading to increased sustainable activity.

Since its introduction, the impact of the green bond on enhancing sustainable activity has been robust. For example, in 2018 the green bond issued by the BBVA Bank in the USA has helped reduce CO2 emissions by approximately 274,000 tonnes, in addition to generating 558 GWh/year of green energy. The resulting rise in green energy uses has helped increase employment in the USA with 0.7 million people currently being employed in the renewable energy industry according to IRENA (International Renewable Energy Agency). This also increases the supply of green energy in the area causing renewable energy prices hit a record low in the USA with energy like wind power being only $28 - $54 per Megawatt Hour (according to the American Energy Information Administration). This makes green energy more affordable for households.

Green bonds seem to be an effective way of stimulating green activity. So, why do they account for only a small percentage of the bond market?

One big reason is the lack of investors’ confidence that funds raised from these green bonds will be deployed to achieve sustainability objectives. Investors have frequently called for greater transparency, disclosure, and standardisation of green bonds to ensure they are used for their stated purpose. Greater clarity over the deployment of funds raised from green bond issues may hence address this lack of market confidence in green bonds.

How can market confidence in green bonds be improved?

One way of boosting confidence would be building greater enforceability and ‘teeth’ into existing regulation around green bonds. This issue is already being addressed by the Climate Bonds2 Initiative (CBI), a not-for-profit organisation aiming to promote large-scale investments towards building a low-carbon economy. The Climate Bonds Standard and Certification Scheme, run by the CBI, allows investors to identify and prioritise low-carbon and climate-resilient investments. The main components of this certification scheme include:

-

Full alignment with the Green Bond Principles3 set by the International Capital Market Association (ICMA).

-

Using best practice for internal controls, tracking, reporting and verification.

-

The assets being financed must be consistent with the goals of the Paris Climate Agreement.

Furthermore, it serves as a marker that assures investors that their money will be going towards the funding of a green project. However, this is currently voluntary, meaning that it is optional for green bond issuers to follow these guidelines. For increased confidence in green bonds, this regulation must be made compulsory by the United Nations and governments with prescribed sanctions for non-compliance or deviations. This could reduce the incidence of fraud in the green bond market and improve security and reliability.

Governments getting deeply involved in the green bond market may be another effective mechanism to address the confidence issue. Governments have often been reluctant to get their hands wet in the green bond market, perhaps due to its relative infancy. But, with the climate crisis on many governments’ political agendas, it seems inevitable that governments (and hence central banks) will venture into the green bond market. This may be done through two ways: government-issued green bonds and asset purchases.

When governments directly issue green bonds, it increases the possibility of the funds raised being used for green projects, perhaps to implement supply-side policies. This is more so since governments could suffer a loss of political support if they were to spend the funds raised on non-green activities. While there will always be room for improvement in transparency and accountability of government spending, such direct involvement by the government may boost investor confidence in these green bonds, thus increasing their demand.

A recent example of this is the NS&I (National Savings and Insurance) Green Savings Bond. This bond, announced by UK Chancellor Rishi Sunak in the 2021 Budget, enables savers to invest their excess disposable income into the funding of environmentally friendly projects via the schemes offered by NS&I. These projects will be executed by the UK Government. Possible projects could include wind farms, revamping public transport and accelerating the transition to electric vehicles. Green government bonds are still in their infancy, and the in-depth details are not available as of now. However, there has been talk of other governments, such as the US government issuing ‘green gilts’ at some point.

Asset Purchases (or Quantitative Easing as it is commonly known) is a third confidence-boosting mechanism. It is what it says on the tin: the central bank purchases market-issued assets such as Green Bonds. Its main purpose is to increase the supply of money in the domestic economy (because a new electronic balance is created by central bank to fund the asset purchase). Here, asset purchases of green bonds would not only increase the money supply but also boost confidence in green bonds. Any central bank typically leads by example in a domestic economy. Hence, the act of central banks purchasing green bonds will enhance the reliability and credibility of these instruments and point the way for other investors to follow suit.

An example of this is the ECB (European Central Bank) increasing their green bond ownership in 2020 from 75 to 115. This increase is likely to spur investors to invest a larger share of their funds into Green Bonds, increasing demand and market share of Green Bonds in the global bond market.

In a nuanced way, asset purchases are starting to stimulate green investment and it will be a crucial way in which central banks can help finance actions to address urgent issues related to the environment and climate crisis.

To summarise, the climate crisis is an existential issue facing us today and the concept of a green bond could be a significant part of the solution to this issue. However, for it to be effective in achieving its objective, boosting investor confidence in green bonds needs to be urgently addressed. Measures such as stronger enforcement of regulation using CBI standards, Governments directly issuing Green Bonds and Asset Purchases (Quantitative Easing) by Central Banks could play a big role in boosting market confidence. This will help increase the demand and market share of Green Bonds. These would in turn drive sustainable activity in the global economy and bring us closer to solving one of the most pressing issues of today.

-

Final Report (2017) on Recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) – Section B ↩

-

Climate Bonds and Green Bonds are the same type of bond. Both increase green activity. ↩

-

Green Bond Principles are a set of voluntary guidelines encouraging transparency in the set- up of a Green Bond. ↩